How Much Does Builder’s Risk Insurance Cost? + Real-World Examples

Discover how much builder’s risk insurance costs based on project type, location, and duration—complete with real-world examples and expert breakdowns.

BUILDER'S RISK SERVICES

Ryan Jones

5/28/20253 min read

Understanding Builder’s Risk Insurance

Builder’s risk insurance is a specialized policy designed to protect buildings under construction. It covers materials, labor, and equipment from unexpected perils like fire, theft, vandalism, and certain weather events. This type of insurance is typically essential for general contractors, developers, property owners, and lenders.

What it Covers:

Damage to on-site materials

Temporary structures

Equipment and tools

Fire, wind, theft, and vandalism

What’s Not Covered:

Earthquakes and floods (unless added)

Employee injuries (covered by workers' comp)

Faulty workmanship or design errors

Key Factors That Influence the Cost

Builder’s risk insurance isn’t one-size-fits-all. Several factors impact how much you’ll pay for a policy:

Project Type: Residential homes usually cost less to insure than large commercial developments.

Location: Coastal or storm-prone areas face higher premiums.

Timeline: The longer the construction period, the higher the cost.

Materials Used: Wood-frame buildings are riskier (and costlier) to insure than concrete or steel structures.

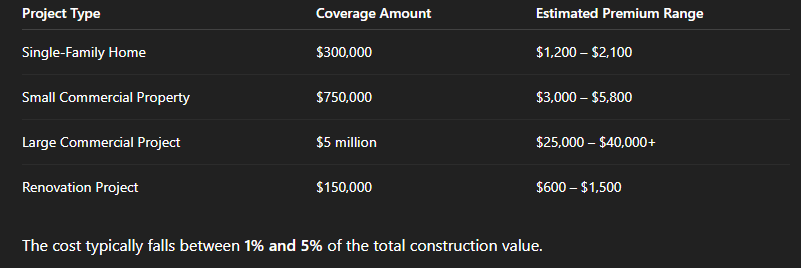

Average Cost Breakdown by Project Type

Here’s a typical cost range based on project types

How Timeline Affects Insurance Premiums

The duration of the project directly influences the premium:

3-6 Months: Lower cost (least exposure)

6-12 Months: Moderate cost

12+ Months: Higher premium with possible policy extensions

Delays can increase costs if coverage needs to be renewed or extended.

Typical Coverage Limits and Deductibles

Most policies offer coverage based on the completed value of the structure, not just material cost.

Standard Coverage Limit: Equal to construction budget

Deductibles: $1,000 to $10,000 depending on risk

Higher Deductibles = Lower Premiums, but more out-of-pocket cost during a claim

How to Get the Best Rates

Here’s how to keep premiums reasonable:

Shop Multiple Quotes: Use independent agents or online platforms.

Specialized Providers: Choose insurers with construction experience.

Bundle Policies: Combine with general liability or workers’ comp.

Hidden Costs to Be Aware Of

Always read the fine print. Watch for:

Extension Fees for delays

Excluded Events like floods or design errors

Permit or Legal Coverage Gaps

Builder’s Risk vs. General Contractor Insurance

Builder’s Risk Insurance:

Covers the structure and materials

General Contractor Insurance:

Covers liability, injuries, and business operations

Many builders carry both, and bundling can lower total costs.

How Claims Impact Future Premiums

Filing a claim can increase premiums. Tips to avoid this:

Invest in site security

Use reputable subcontractors

Regular safety inspections

Loss-prevention measures often lead to discounts or reduced deductibles.

Builder’s Risk Insurance for Renovations

Renovation projects bring special risks:

Occupancy risks if owners live on-site

Partial structure creates coverage gaps

These policies usually cost less than full new builds, but need careful structuring.

Choosing the Right Insurer

Top U.S. providers for builder’s risk insurance:

The Hartford

Travelers

Nationwide

Chubb

Questions to ask:

What perils are covered?

Can I extend my policy if delayed?

Do you offer bundling discounts?

Frequently Asked Questions (FAQs)

1. How much does builder's risk insurance cost per month?

Most policies are charged as a lump sum, but monthly breakdowns can range from $100 to $800+ depending on project value.2. Is builder’s risk insurance required by law?

It’s not legally required, but often mandatory for loans or by local building regulations.3. Can I cancel my policy early if the project finishes sooner?

Yes, but you may only receive a partial refund, depending on the insurer.4. Are subcontractors covered under my policy?

Usually no—each subcontractor must carry their own general liability coverage.5. What happens if I underestimate my project value?

You risk being underinsured, meaning any claim might not fully cover damages.6. How long does a builder’s risk policy last?

Typically matches the construction timeline—3 to 18 months, with options to extend.Final Thoughts

Understanding how much builder's risk insurance costs involves analyzing your project's scope, location, duration, and materials. While prices vary, being proactive with safety, bundling, and selecting the right insurer can lead to meaningful savings.

Builder’s risk insurance isn’t just a cost—it’s a smart investment in the success of your construction project.

By Rye and Friends

Your trusted partner for business insurance solutions.

contact

request A quote

© 2025. All rights reserved.

SERVICES

Builders Risk / Course of Construction